The story line of 2023 is taking shape and that is one of stop and go. The winter had movement, then the wet spring effectively put a pause it. In June, inventory came relatively roaring back, and thus our number of pended listings should strengthen the total sold volume in the third quarter. Thus, the second quarter was about building back up and leaves me suspecting that we could have a later selling season, i.e. a decent amount of movement moving throughout the fall.

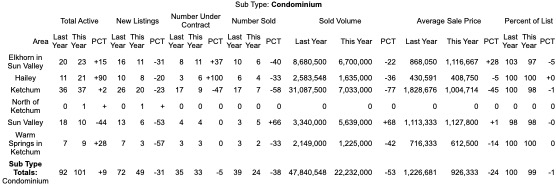

In the condo world the second quarter is picking of speed and developing its own ’23 version of momentum. From the amount of inventory active and the number under contract everything points towards a big third quarter. Lots of units have gone under contract in the second quarter they just haven’t closed yet to impact the number of units sold, sold volume, and the average price. At the moment, the fact that the average price is down 25% from the second quarter in ’22 is good for buyers and the fact that condos are selling for 99% of their list price means sellers are pricing well and getting what they’re asking.

If we look at Ketchum, on paper inventory is nearly flush from a year ago and still the total dollar volume is down as is the average sales price. If the average sales price is down then in theory this should fuel a higher total volume. Not that is should meet the same amount from a year ago, but it should be bringing more buyers to the frontlines. Instead, since this isn’t the case, our inventory either consists of more high end product or pricing that doesn’t match what the market is willing to pay. This theme will come back again.

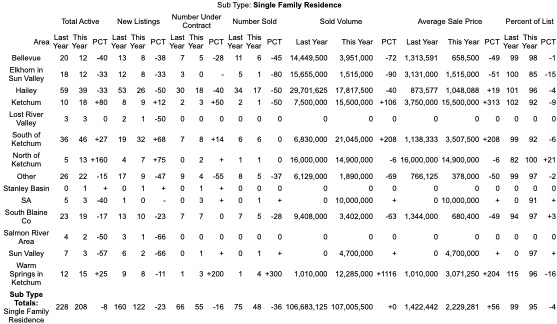

In single family homes, the Warm Springs market is now blending into Ketchum. This makes sense and in the past, they have been fairly segregated markets from one another. Buying and pricing trends at the moment point to them becoming equals. Total volume is very healthy and a hair above 2022 if you can believe it. Still, the average price is up 56% so it doesn’t take as many sales, 36% less, to have a substantial amount of volume. 95% sale to list says to me that sellers aren’t willing to risk leaving money on the table so throw a number at em and see what sticks because clearly some are.

On an additional note, the rising average in Hailey is putting pressure on the Bellevue market. Though the numbers from the second tell us that their average is down and so isn’t their total volume so my suspicion is that of the Ketchum condo market.

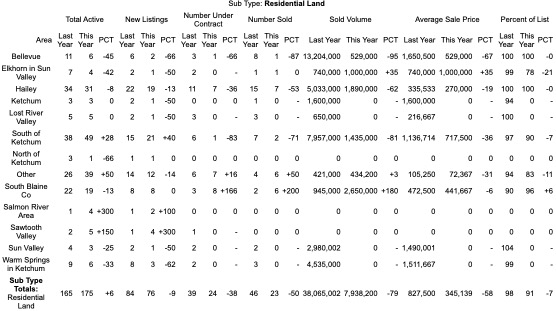

In land, much like condos, is having a slow start and will come back in its own way as the pended parcels in the second quarter close in the third. At 91% sale to list price tells me that some buyers are having some fun throwing contracts out there looking to see what will stick. I might be representing some of these efforts. Surprisingly, Bellevue doesn’t have a whole lot to offer where it usually did.

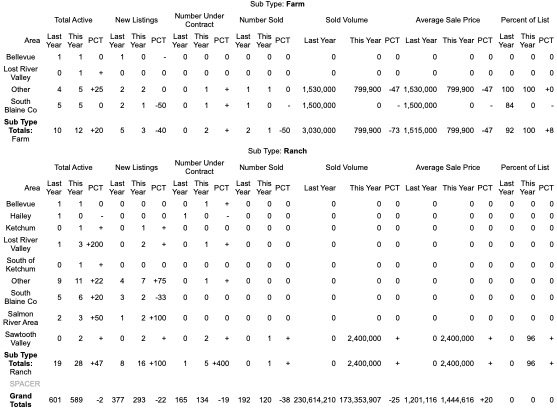

In farming, inventory remains even and should start reflecting higher total volume once the two pending farms close. Ranches are making a pretty good push especially compared to a dormant second quarter in ’22. Still, we’re talking about moderate ranch sizes and capabilities. Truth of the matter is at the moment the real deal stuff available are not listed.