2022 should be categorized as the year of the shift. Even though ‘22’s winter was slow it did pull in 2021 prices. April first was the cut off and was the beginning of how we know it now. The story of ‘22’s slow down had a lot to do with prices staying high as inventory, though it was down, wasn’t down by much for the most part. Climbing interest rates paired with relatively low inventory and you really have to go looking deep to find where supply and demand curve meet on paper.

Unfortunately, the biggest hits were most commonly in sectors furthest away from the epicenters or community cores. Market activity encouraged rare property to come on at big numbers only to sit tight for the most part. 2022’s story has many and I attempt to divulge them below.

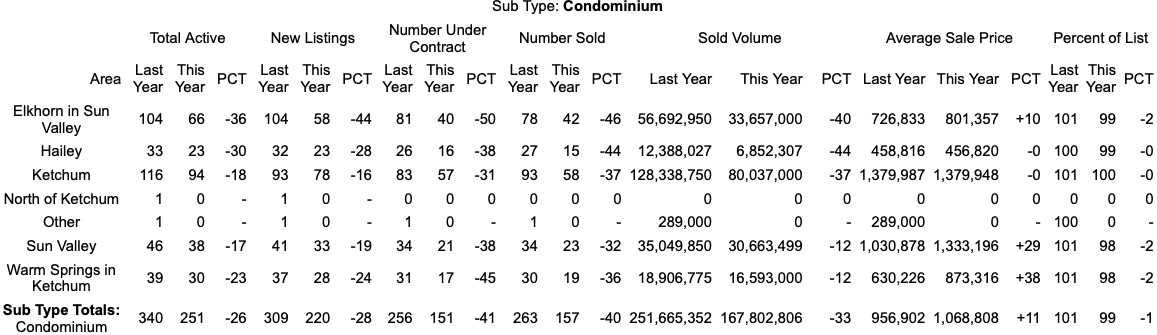

The Condo market for the year of 2022 took a hit for the most part and I argue that this largely has to do with a lack of available inventory in the Elkhorn area. They were down 36% which translates to 38 less units which makes up the largest amount lost when comparing ’22 to ’21. As a whole inventory was down 26%, 340 units in ’21 and 251 in ’22. This measurement alone carries thematically throughout the rest of 2022’s statistics. 40% less condo units sold in last year and led to a decrease of 33% in total sold dollar amount. On the other hand, the average sale price was up 11% and this was due to Sun Valley and Warm Springs taking a 29% and 39% leap in their average sale prices.

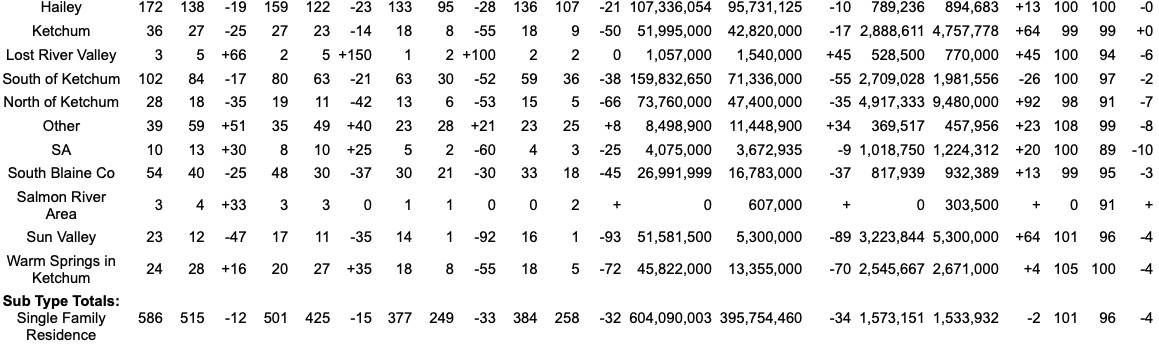

Single Family in a nut shell, had their total volume dollar down 34% this year. From 604m to 395m. The average sale price came down 2% and units are selling for an average of 96% of ask. Here’s where the story breaks down: in Bellevue only 50 homes sold versus 70 the year before and I would say this had to do with a lack of new inventory. Still, only 12% less in total dollar volume as their average price came up 25%. Hailey continued to be active and reported 19% less active homes. Their price came up 13% which is why their total volume was only down 10%. Ketchum was surprisingly low with only nine homes selling this year. Their numbers for the most part were down across the board but wouldn’t you know their average price was up 64%. So, just big stuff selling. Mid Valley slowed down pretty hard despite healthy inventory. Sun Valley was in a similar boat with their one sale of the year. And Warm Springs took a bit of a monster hit with 70% less totally volume sold. Total inventory was only down 12% for the year and there were still 515 total homes for sale. Aside from Bellevue I would argue average sale prices still climbing was the blame for inactivity. Elkhorn on the other hand defies the entire market as they had 15 more homes available this, 32 of them were new to the market, sold volume was up 39% and their average sale price was up 50%!

Vacant Land’s story is fairly similar to single family homes in that prices were up so number of sales went down. Inventory never really came up in any area of the market so not a surprise. It stayed tallied 325 total units from 508 the year before, that’s 36% less. 135 total units sold throughout the year whereas in ’21 there was 356 and the average list price was 780 versus 390 a year ago. Price, lack of new product, and construction costs probably have everything to do with this.

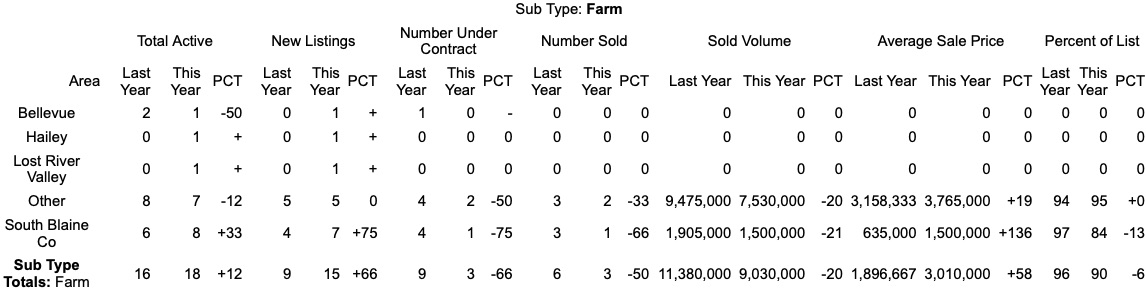

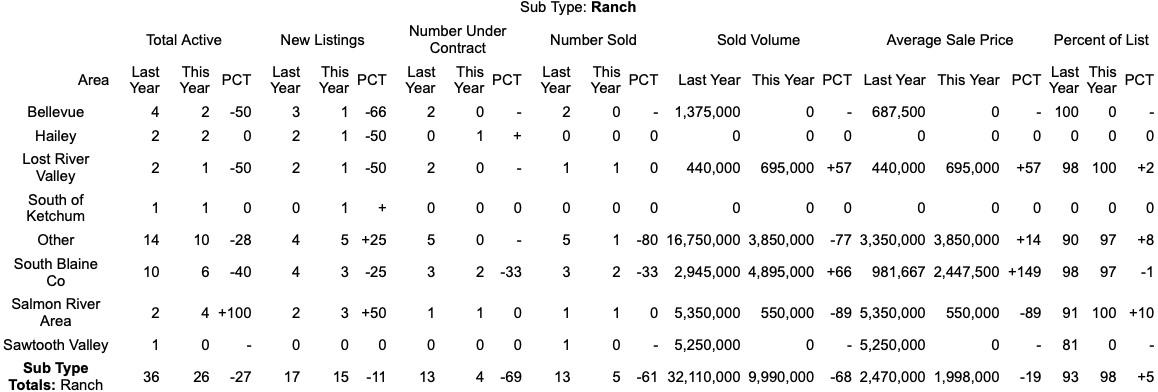

Here's the skinny on Farm and Ranch. A brief one and considerable. Six farms sold this year, that’s half as many as last year despite having 18 actives versus 16 a year ago and of the 18, 15 of them were new listings. Despite less sales the total sold dollar volume was around 9 million from 11.3 a year ago, only down 20%, which means the average sale price was 3m from 1.9 and selling at 90% of asking. The ranch world did not prevail as strong. It had ten less listings this year at 26 and from 36 and only five sold versus 13 in ’21. Their total dollar volume sold was down 68% at just under 10 million and the average price was down 19% at about 2m from almost 2.5 the year prior. They were pulling 98% of asking this year however from 93% a year ago.